The Merger Effect: Banking in Georgia

Mergers and acquisitions create new opportunities in Georgia, even as community banks feel the squeeze.

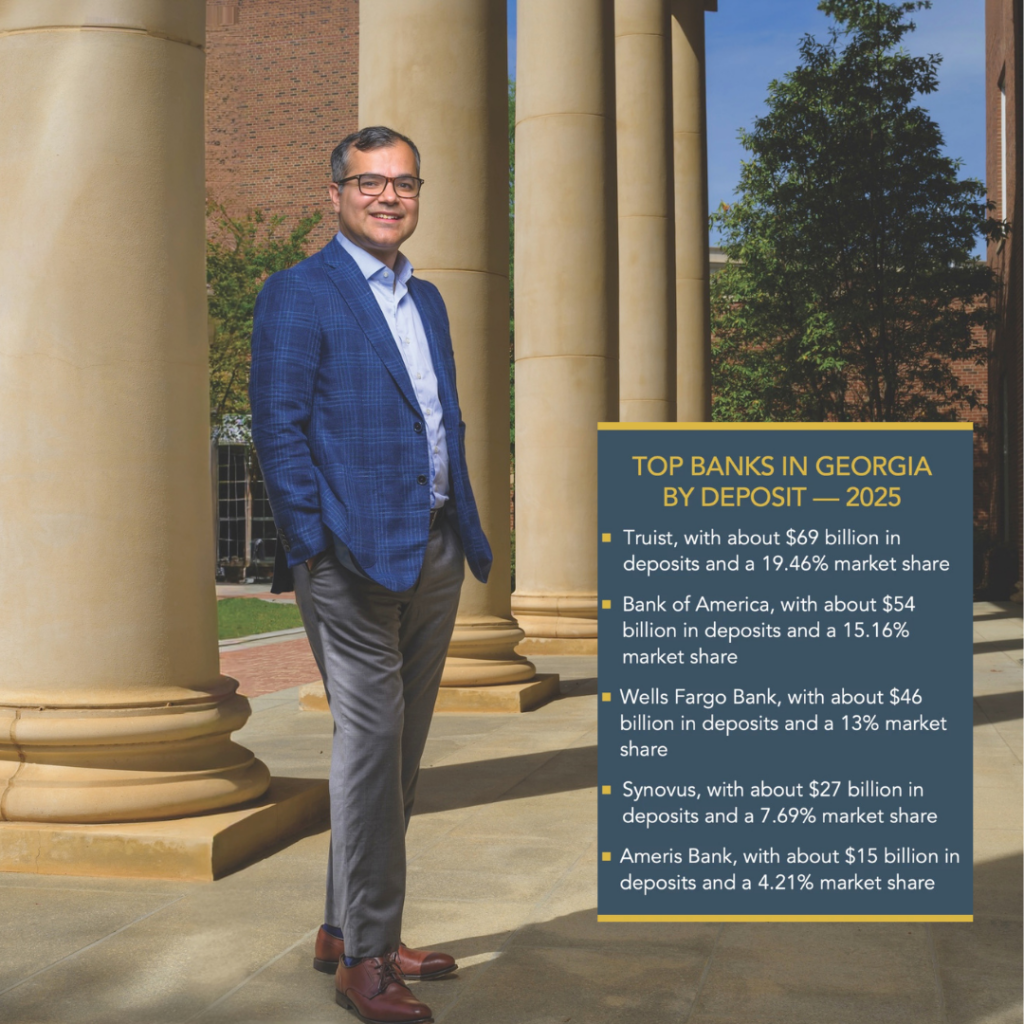

More Consolidation: Siddharth Vij, assistant professor of finance in the Terry College of Business at the University of Georgia. Photo credit: Daemon Baizan

The May 2026 issue of Georgia Trend included a banking feature titled “The Merger Effect” that contained numerous errors regarding Pinnacle Financial Partners, which has merged with Georgia-based Synovus. The portion about eliminating back-office duplicate positions misrepresented Charlie Clark’s statements about limited overlap between the two banks. As Pinnacle has stated on the public record many times, personnel impact is expected to be five percent or less. Furthermore, we mistakenly stated that Pinnacle merged with Morris Bancshares prior to the Synovus merger. Pinnacle Financial Partners has no relation to the Pinnacle Bank in Northwest Georgia, which announced a merger with Morris Bancshares and name change to Vallant Financial earlier this year. Other errors have been corrected in the online version of the article. We regret the errors and take full responsibility for their publication.

————————-

Banking in Georgia had a busy 2025 that continued this year with the $8.6 billion merger of Synovus Financial and Pinnacle Financial Partners, making the state a leading player in the red-hot national trend toward bank consolidations.

The deal between the Columbus-based Synovus and the Tennessee-based Pinnacle Financial, announced in July 2025 and completed in January, is part of a national wave that saw at least 180 mergers nationwide since the beginning of 2025, including at least three in Georgia.

“The big trend not just in banking in Georgia, but nationwide, is consolidation,” says Siddharth Vij, an assistant professor of finance in the Terry College of Business at the University of Georgia who specializes in banking and corporate finance. “Banking has gotten a lot more nationalized.”

That recent consolidation has cut two ways for Georgia. On the one hand, consolidation has made some banks bigger and stronger and opened the way for out-of-state institutions to do business in Georgia. But these consolidations also have forced some local smaller banks to shrink as they close branches. They have even ended up forcing small banking companies out of business.

Bank mergers have been occurring for decades but had slowed between 2022 and 2024 due in part to tighter regulatory oversight by the federal government. That has changed under the Trump administration, with the highest level of approvals last year since 2021 and at the fastest pace since 1990, the Financial Times reported in November.

“There’s some pent-up demand. Now we’re getting into more of a favorable regulatory environment,” says Charlie Clark, who heads Georgia banking for Pinnacle Financial Partners.

Faster Mergers: Charlie Clark, head of Georgia banking for Pinnacle Financial Partners, which merged with Columbus-based Synovus Financial. Photo credit: Daemon Baizan

Clark was named to the post after the merger in January; he had worked for Synovus for nearly 20 years, most recently as president of community banking.

“We’re now the largest headquartered bank holding company in the state of Georgia,” says Clark, who had been based in Birmingham, Alabama, but is now working from Atlanta.

The holding company, Pinnacle Financial Partners, has more than $117 billion in assets. Pinnacle Bank is its prime subsidiary. Pinnacle-Synovus was one of the biggest consolidations announced in the nation last year, behind a $23 billion merger between OceanFirst Financial and Flushing Financial expected to close this summer, and a $10.9 billion deal between Fifth Third Bancorp and Comerica, which closed in February.

“Consolidation is something that has certainly accelerated. It feels more routine within banking,” says Mary Beth Coke, the Atlanta-based executive vice president and commercial banking district director for Regions Bank, which is headquartered in Birmingham.

2025 Deals

While the deals were not as large as the Pinnacle/Synovus merger, a number of other banks consolidated in the past 18 months. For example, the Georgia Banking Company ($2.7 billion in assets) acquired the Tucker-based Tandem Bancorp ($304 million in assets). That merger became finalized in February. And in January, Century Bank and Trust acquired Bank of Wrightsville. In 2025, deals in Georgia included:

- the acquisition by First Community Corp. of the Sandy Springs-based Signature Bank of Georgia for about $50 million

- the acquisition of Trenton-based TAG Bancshares by Alabama-based CBS Banc-Corp

- Fitzgerald-based Colony Bankcorp obtaining Thomasville-based TC Bancshares.

One of the main reasons banks consolidate is that they grow faster by acquiring than by organic efforts. They also seek to mitigate the increasing costs of technology, cybersecurity and regulatory compliance.

“For some banks, the merger makes sense because you can eliminate redundancy,” UGA’s Vij says. “For other banks, the merger … makes sense because it grows the size of each bank.”

The Pinnacle-Synovus deal merged each bank’s strengths, notes Clark, who has worked for both institutions. Pinnacle was a commercial bank with a large number of high-dollar business accounts but only a handful of branches in Georgia.

Synovus had offices in nearly 100 locations in Georgia, making it one of the largest regional banks in the state, according to Clark.

“Now that we’re coming together, we can do it on a much bigger scale with a broader footprint,” he says.

The combined banks have more than 400 locations across Georgia and eight other states.

Except for back-office functions such as technology and computer systems and human resources, Clark says he sees limited overlap.

The merger should be complete in early 2027.

“The big trend not just in banking in Georgia, but nationwide, is consolidation. Banking has gotten a lot more nationalized.” – Siddharth Vij, assistant professor of finance, University of Georgia’s Terry College of Business

Regulatory Matters

Some financial institutions in Georgia are bucking the trend and are not consolidating at this point. Truist Bank, which is the largest in the state with more than 19% of the market share and about $69 billion in deposits in 2025, has not signaled any merger plans – beyond the formative one in 2019. Truist was created from the merger of BB&T and SunTrust Banks and now has 203 branches statewide.

Scale Matters: Katherine Saez, Georgia and Alabama regional president for Truist Financial Corporation. Photo credit: Daemon Baizan

“We’re focused on ourselves right now,” says Katherine Saez, Truist’s Georgia and Alabama regional president. “And when I say focused on ourselves, we’re focused on executing the strategy that we’ve laid out.”

Saez says Truist had substantial uncertainty last year about regulatory matters.

“Scale matters. It allows you to invest in technology, which is so critical in the banking space. But one of the things we realized and leaned into here at Truist is that, yes, scale matters, but strategy matters more,” she says. “So, the strongest banks are those that are investing not just in technology, but also client, communities, talent and the strategy that goes behind that.”

Truist made a major statement as anchor tenant of The Battery; its office there is officially known as Truist at Five Ballpark Center. Bank officials are happy to point out that the nine-story, 250,000-square-foot building is 300 feet from the Atlanta Braves home plate at Truist Park. Nearly 800 Truist employees work at the building, which had a groundbreaking in 2022 and was completed in July 2025.

Branching Out

Regions Bank also is not planning any immediate merger or sale, says Coke, the executive vice president. It is planning changes, though. CEO John Turner announced in mid-March that the bank has sped up plans to build at least 135 branches in Georgia, Florida and Tennessee during the next five years. It had initially been a seven-year plan. But Regions simultaneously will close about the same number of branches, as the bank responds to population shifts and combines two or three branches into one. Regions executives say they’re responding to market changes caused by the consolidations. This should benefit customers as well as employees, the executives say.

“We’re viewing the disruption as an opportunity for our bank,” Coke says. “What is incredibly beneficial to a bank that is not going through some of the merger noise is that we provide a very stable, well-heeled platform that can be a safe area for those that have been impacted or are fearful of being impacted. … This should give us some opportunities to differentiate ourselves.”

Coke says she joined Regions about two years ago, after working at a bank that went through a merger.

Coke says she joined Regions about two years ago, after working at a bank that went through a merger.

“I can speak from personal experience about some of the stability [issues] that I’m discussing,” she says.

JPMorganChase, the largest bank in the nation, also is not involved in any immediate mergers or acquisitions although it is adding branches in Georgia, says Roxann Cooke, regional director of Consumer Banking for Georgia and North Florida. By the end of next year, the bank plans to have 115 branches in Georgia and more than 2,000 employees across all lines of business in the state.

“Where consolidation creates gaps, we evaluate opportunities thoughtfully – guided by data and community needs – to add locations and services responsibly,” Cooke said in an email. “The objective isn’t just more locations; it’s the right mix of branches, ATMs and digital tools so Georgians have practical, reliable access to banking in the neighborhoods that need it most.”

Concerns and Challenges

The mergers have hit small community banks the hardest. Local banks have long been anchors of small-town and community lending, but that paradigm is slipping away. Regulators play a role, as they prod consolidation between regional and community banks. After a merger or acquisition, overlapping bank branches, particularly those in remote or low- to moderate-income areas, are often closed. And although merged banks can offer more online and mobile banking tools, some residents in these areas don’t have access to that technology. The nearest branch can be many miles away. That’s a major concern for John McNair, president and CEO of the Community Bankers Association of Georgia.

“The mergers have been a challenge,” he says. “Back in 2008, 2009, Georgia had about 350 banks chartered in the state. There are 159 counties in Georgia. We had one bank headquartered in every one of those 159 counties.”

At the beginning of 2025, there were 114 state-chartered banks headquartered in Georgia, according to the state’s Department of Banking and Finance. McNair says he would like regulatory policy implemented to provide incentives to local business owners to start banks in their communities. Incentives could be accomplished at the state and federal levels, he says.

Local business leaders also can come together and start their own banks, he notes. That’s what Moultrie Bank and Trust did when an investor group attracted 486 shareholders and raised around $21.5 million in capital to open the bank in May 2022. But community banks face another threat. Credit unions also are acquiring local banks. As of January 2025, there were 36 state-chartered credit unions in the state.

“Credit unions have a regulatory advantage,” McNair says. “They don’t have to comply with what’s called the Community Reinvestment Act, which requires loans to be made to people with certain income levels. They are also exempt from state and federal income tax. So, a credit union buys, essentially, a community bank with taxpayer dollars.”

Large banks promise to maintain a focus on communities. Over at Pinnacle Bank, Clark says his institution can fill the void.

“Consolidation is something that has certainly accelerated. It feels more routine within banking.” – Mary Beth Coke, executive vice president and commercial banking district director, Regions Bank

“We’re really focused on empowering our local leaders, and so, if you look across the state of Georgia, we’re in markets like Tifton, Valdosta, Albany, Thomasville. And, in a lot of these markets, we’ve got [the] No. 1 market share,” he says. “And so, we’re going to do all we can do to protect those communities, those markets. And, in the shift to the Pinnacle model, where we put more authority in those local markets, it’s going to really set us apart to not only show our commitment to those communities, but we’re also able to bring better technology and solutions to those communities. We’re positioned to be the dominant force in all markets in Georgia that we currently reside in.”

Despite moves by larger banks, though, some community banks remain viable.

“On this banking desert issue, we’re not quite there yet in Georgia,” McNair says. “But it is a problem.”

Community banks have the advantage that they know their market and know their customers.

“Community banks are small business lenders,” McNair says. “That’s what they do – the local barber shop, the pizza shop, etc.”

“The strongest banks are those that are investing not just in technology, but also client, communities, talent and the strategy that goes behind that.” – Katherine Saez, Georgia and Alabama regional president, Truist Financial Corporation

UGA’s Vij notes that means community banks play a vital role locally, even if it is diminished. “In the old days,” he says, “the advantage that small banks had was that the loan officer was in the community. He knew small businesses. A small-town banker knew everyone in the community.”

McNair sees a narrow path for community banks to remain healthy if they’re not gobbled up by larger institutions.

“A lot of senior citizens are not invested in the stock market,” he says. “Their funds, their retirement savings are in six- to 12-month CDs at their local bank. And, if a bank can pay 3.5%, 3.75%, then it’s kind of a low rate, but it’s a fair rate relative to what inflation is now. And if it lends money out at 6.5% [to] 7%, those are pretty good spreads. They’re making those loans and they’re doing just fine.”

Mergers remain a threat, though.

It’s unlikely that community banks will become extinct, McNair says, but he predicts that within the next five years, fewer than 100 will remain in Georgia.

Regional banks moving into community markets can still make a positive difference, he says.

“Some of them are very smart. They’re putting local decision-making here. So credit decisions can be made here versus going back to Charleston or Charlotte or Memphis or wherever,” says McNair. “They’re not filling the void completely, but they’re doing a good job. And a lot of the banks are from out of state; they’re good, well-run, well-capitalized institutions. So we welcome them here.”

Welcome to the Future

The future has arrived for Georgia banking: Artificial intelligence, better known as AI, is making banking easier, faster and more economical for customers as well as financial institutions.

The future has arrived for Georgia banking: Artificial intelligence, better known as AI, is making banking easier, faster and more economical for customers as well as financial institutions.

“With regard to the speed at which AI is impacting many markets and businesses, including banking – it’s unlike anything I’ve ever seen,” says Mary Beth Coke, the executive vice president and commercial banking district director for Regions Bank.

University of Georgia Assistant Professor of Finance Siddharth Vij says, “It’s a level of sophistication and amplification that didn’t exist before.”

AI brings benefits for customers as well as bank employees and the banks themselves. Customers have easier and quicker access to information through online and telephone queries. Gone are the days of being asked to press 1 for one topic, press 2 for another and press 3 for something else. These days, customers state a question and an AI bot interprets it and searches its database for an answer – all within seconds. Al McRae, president of the Bank of America Atlanta, says he has seen a 50% reduction of clients calling customer service to speak with someone about requests or problems.

“We are enabling our clients so much with these different tools and technology,” he says. “So, we can see the benefits on that end.”

But AI also helps the banks and its employees, McRae says, with “the enablement of our associates to utilize these tools to help them do their jobs quicker, faster, in a more efficient way.”

Coke also touts AI’s efficiency.

“It has an ability to be predictive around future demands,” she says. “Patterns, trends, things that we may not be able to see as rapidly or as real time as AI is able to deliver to us.”

And it can highlight a customer’s individual needs.

“Our bankers have adopted it rapidly and use it daily,” Coke says. “In fact, I use it daily. And it drives measurable results because you’re able to look at your platform or your portfolio of clients and, in a moment, identify where there’s potentially a client that needs some attention.”

Charlie Clark, who heads Georgia banking for Pinnacle Financial Partners, also points to how AI can help bankers help clients.

“It’s really about how do we provide better information to our team members so that they can provide better advice to the clients, and, therefore, we deliver better returns to our shareholders,” Clark says, adding it’s not about eliminating jobs.

Katherine Saez, Georgia and Alabama regional president for Truist Financial Corporation, also sees AI as vital component of modern banking. She says Truist is using AI for customer service, investment banking and fraud prevention.

“We believe we have to invest in AI not just to create operating leverage and efficiency, but to really derive a better client and teammate experience,” she says. “Around here, we often refer to it as augmented intelligence – not to replace people, but to help people do their jobs better – whether that’s more efficiently, more effectively, have better experiences.”

Artificial intelligence at JPMorganChase, the largest bank in the United States, gives its approximately 318,500 employees safe, flexible tools for writing, summarizing, solving problems and generating ideas, says Erin King, the bank’s chief information officer for commercial banking.

“Broadly speaking, we use AI to support fraud detection, sanctions screening, trading, operations, document processing and regulatory compliance,” King said in an email, adding “what once took hundreds of hours now takes fewer than 20.”

Vij says there will soon be even more uses for AI.

“It’s one of those things where everyone is still trying to figure out the best use of this [new technology],” he says.