The Perils Of Prosperity

A booming economy and a hot housing market have made Georgia a leader in subprime lending and in mortgage fraud and foreclosures. Some lenders consider the recent turmoil a market correction and say additional regulation could do more harm than good.

For the mortgage banking industry in Georgia, the bill has finally come due. And it’s a balloon payment.

Stories of subprime mortgages gone bad are rampant, and the effects are being felt by lenders, brokers, banks, builders and, ultimately, retailers and service industries – as well as individual homebuyers.

The subprime debacle has been likened to a torpedo threatening the entire economy. Subprime loans, so named because they are designed for customers with less-than-desirable credit ratings, are the specialty of big national operations – many based in California – that loan money in every state, including Georgia. Nationally, at least 30 such companies have gone under already this year.

Georgia has led the nation in subprime lending – and in mortgage fraud and foreclosures.

The trouble here started with prosperity: a booming economy, a hot housing market, phenomenal growth. All this success attracted a host of newcomers to the mortgage banking business – an emerging industry which until the 1990s had been largely unregulated everywhere. Georgia has seen perhaps its biggest influx of ambitious newcomers seeking to take advantage of economic opportunity since the carpetbaggers of reconstruction. Some have been too aggressive with lending guidelines, and some have been outright criminal.

“We’ve had the honey to attract the flies,” says Rob Braswell, commissioner of the Georgia Department of Banking and Finance, which regulates state chartered banks, credit unions, mortgage lenders and money transmitters. “There’s a lot of money to be made in mortgages. We’ve heard that former drug dealers have gotten out of the drug business and into mortgages because they could make just as much money without the danger.”

That might not be such a good idea these days, though. Georgia grew tired of being number one in the country for mortgage fraud – for three years running. The banking commissioner and his staff joined forces with law enforcement, the state attorney general and a citizens group called the Georgia Real Estate Fraud Prevention and Awareness Coalition.

Last year, the state issued 108 cease-and-desist orders and 17 notices of intent to revoke licenses – all for mortgage fraud alone.

“In 2005, we dropped from number one for fraud to number three in subprime and number five in the prime market. We’re very pleased,” Braswell says. “That doesn’t sound like a big drop, but we do know the amount of fraud has decreased.”

The commissioner expects that this year Georgia’s mortgage fraud statistics will drop to near the national average. “We’re seeing results,” Braswell says. “We’re not satisfied, but we’re very encouraged.”

The state has only been regulating mortgage lenders since 1993, when the General Assembly passed the Georgia Residential Mortgage Act. This was a response to the boom in the mortgage business that began in the 1980s, fueled by falling interest rates and rising home sales. Before that, most people got their mortgages through traditional banks that favored traditional terms, such as 30-year fixed rates with a down payment.

But as demand grew, more people got into the business. Mortgage-only lenders began to grow. And brokers began attracting customers and finding them lenders in the same way real estate agents court buyers and shop around for a house.

Meanwhile, Wall Street lit a fire under the business as investors sought the high returns of mortgage-backed securities. All this created pressure to get more and more people into mortgages – even those who couldn’t afford the traditional terms. The guidelines slackened and the risk increased. Defaults, foreclosures and fraud grew exponentially.

But even though Georgia took steps to regulate the industry in 1993, it took time to move the bureaucracy. It wasn’t until 1998 that the state’s banking and finance department got its first full time mortgage examiner, Rod Carnes, who is now deputy commissioner for non-depository financial institutions. Carnes’ division currently has nine mortgage examiners.

Aside from fraud, most of the trouble in Georgia and much of the country has been triggered by the mushrooming market for nontraditional subprime mortgages. But next in line on the risk scale are so-called Alt-A loans, which go to customers whose credit is better than subprime, but not quite prime either. Alt-A has come into wider use as well, along with other higher risk business: adjustable rates with balloon payments; teaser loans, which offer a lower than market interest rate at first and then jump up after a year or two; mortgages for 100 percent of the value of the home – sometimes even 125 percent. Apart from outright fraud, these would be the cause of most of the foreclosures, Braswell says.

Unfortunately for Georgia, such loans have accounted for much recent business. “In Atlanta, 55 percent of new mortgages in 2005 and 2006 were the exotic kind – nontraditional,” says Braswell, the banking commissioner. “Those type mortgages are coming home to roost.”

Another reason Georgia has led the nation in foreclosures is simply that it’s easier for a lender to foreclose here. State law allows for relatively quick foreclosures – 37 days after a default.

More Regulation?

All this has led to talk at the state and federal level about possible changes to laws and regulations governing mortgage banking. But responsible voices in the industry advise caution.

“The regulators are coming under fire from Congress, which is asking how did we allow this to happen,” Braswell says. “Regulation is reactive rather than proactive. If we stop it [nontraditional lending] then we’re cutting off credit. How far do we step in to tell people that government knows best?”

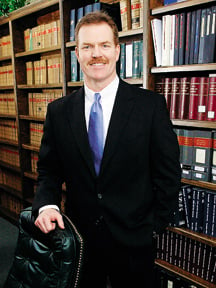

The perspective of many mortgage industry leaders is that the defaults and the downturn in business show the natural way the economy fixes problems. “What the banks and lenders are seeing right now, the slowdown, is a market correction,” says Tyler Wood, president of the Macon-based Mortgage Bankers Association of Georgia.

Wood speaks from experience. He and a group of partners opened an Atlanta-based mortgage company called SouthStar Funding in 1998. In nine years, the company expanded into 50 states with 600 employees. Last year, the company originated more than $6 billion in mortgage loans. This year, it went bankrupt. The company had to close its doors in April when major investors demanded that it take back loans that SouthStar had originated, bundled and sold on the secondary mortgage market. Those loans amounted to considerably more than the company’s capital reserves.

The same scenario is playing out around the country as Wall Street tries to extricate itself from the subprime and Alt-A troubles in the secondary mortgage market. Says Wood, “The market has corrected itself.”

Wood’s partners are personally protected from the company’s bankruptcy, and they held onto their capital by closing their doors. Wood himself made a lucky decision three years ago to sell his interest to his partners so he could move back to his hometown, Macon, to be near his parents. He was working for the company in Macon as executive vice president and director of governmental affairs. Now, he is shopping for health insurance and his next job. He plans to stay in the mortgage industry.

“It’s a great business – when it’s good,” Wood says. “It’s a good business even when it’s bad.” But the severity of a downturn is in direct proportion to the extent of the boom in the good times.

“I hope Congress doesn’t make a hasty decision with intense legislation because the market has already reacted and heightened the guidelines,” Wood says. “There is not a need for government to step in.

“I have trouble when you start to play with the market, play with the economics, having someone unfamiliar with our industry making that decision,” Wood says. He suggests that passing overly restrictive laws can lead to investors pulling out of a state and damaging the entire economy.

“The industry goes in cycles. We’ve come off one of the best runs in the history of the industry,” Wood says. When the boom peaked in 2004, mortgage loan production was up to $4 trillion for the nation. The forecast this year is about half that high, around $2 trillion.

Those in the strongest positions in Georgia’s mortgage industry are the businesses that have waded less deeply into nontraditional loans, such as Atlanta-based HomeBanc Corp., which closed $6 billion in loans just last year.

“The industry was “lulled into a false sense of security because real estate values were rising,” says HomeBanc CEO Kevin Race. “There are going to be significant delinquencies. There will be market impact. Investor standards around people’s ability to afford mortgages are going to be tightened. Credit standards are going to be tightened.

“The key for us is, are you really exposed to that or just affected tangentially? Only less than 1 percent of our business is subprime. We’ve always focused on prime lending. We have a real opportunity while a lot of competitors are focused on problems, distracted.”

Looking Ahead

While others may be working on staying in business, HomeBanc is looking ahead to creating new strategies for growth. The CEO is interested in affinity group marketing, vertical housing, expansion of condominium ownership even outside the big cities in the four states where HomeBanc does business. “The industry is going to become more normalized after a hyper market,” Race says.

Others among Georgia’s blue chip giants also see opportunity in the downturn.

“There’s a real flight to quality – quality products and quality lenders,” says John Pruitt, senior vice president and Atlanta regional mortgage manager for Georgia-based SunTrust. He describes the industry in general as “highly unregulated,” and says, “It’s pretty darn easy to get into the mortgage business.”

It is getting harder to stay in the business, however. But complaints about predatory lending practices, fraudulent and incompetent brokers and mortgage nightmares flooding the internet and regulators’ offices may strengthen the position of reputable institutions.

“The quality players are surviving and even flourishing. Now is when we’re seeing our market share improve,” Pruitt says. “We truly look at this correction in the market as an advantage for franchises like SunTrust that have been here and are going to be here.”

A bank that offers mortgages takes a different view of the business than a mortgage company, Pruitt notes. The mortgage business is a significant portion of the total company’s earnings, but it’s possibly even more important because it brings customers into the bank. “In a lot of ways, the mortgage is the entry of the customer to the bank franchise,” he says. Also, a diversified financial institution won’t be so vulnerable when mortgage activity does decrease – either due to interest rates climbing or home sales falling.

Those expecting to stay in the business don’t seem to mind a shakeout among competitors. “If things get tough, all the idiots leave. If things start booming again and there’s a lot of low hanging fruit, they’ll get back in,” says Mike Maniaci, owner of Piedmont Mortgage in Atlanta. “What really concerns me is whether people are buying houses. There’s some refinancing, but that has slowed. And the housing market has slowed down.”

And there’s the rub: the pressure created by a slowdown in housing purchases and refinancing. Part of the problem with the burgeoning mortgage industry was that when business began to fall off after the peak in 2004, pressure remained to keep the volume up. That’s when underwriting standards really eroded to keep up the volume, according to Georgia’s banking commissioner.

“The way the industry is structured, there’s incentive for everyone to make the loan, starting with the consumers, who might want to get into a house that’s a little above their means. Then there’s the broker, who wants to get the fee, and the mortgage lender, who wants to make the loan. And the lawyer wants to close the deal,” Braswell says. “Then there’s Wall Street.”

Much trouble is being blamed on pressure from the flood of available investor money. Even high risk, nontraditional mortgages have been considered good investments because of the 89 percent or so of homeowners who could be counted on to make their payments on time. But if Wall Street has been seductive, lenders, brokers and buyers have been too willing to go along.

The banking commissioner and the deputy commissioner for mortgage industry talk about the oft-repeated scene at the closing table where there’s never a voice to say to the buyer, “Hey, is this really such a good idea? Slow down. Can you really afford this? What happens when the adjustable rate goes up, the balloon comes due or the real estate values don’t rise enough to cover the 125 percent?”

Still, mortgage lenders like to note that home ownership has soared to record heights during the mortgage boom of the 2000s – even among groups that traditionally have not owned their own homes. Among African Americans and Hispanics, home ownership is up to 50 percent in Georgia. HomeBanc, for example, has created separate divisions to court the business of minority communities, seeing opportunity in helping them move upward toward the near 70 percent rate of home ownership among majority populations.

When all is said and done, home ownership is still the fabric of the American dream.

“That’s one of the reasons why I loved going to work every day,” says Wood of the Mortgage Bankers Association of Georgia and the now-bankrupt South-Star Funding, who plans to get back in the business as quickly as possible. “The most fun part of the job was the buyer – especially when it’s the first home. Yes, there was an excessive amount of capital available in the marketplace, but there’s also the story of folks being able to get in and purchase a home and being very pleased.”